16.04.2024

The ECB as a Palliative to Europe’s Political Quagmire

Tribune

19 avril 2017

As it became increasingly clear, as early as 2011, that Berlin would not accept the kind of public debt pooling that most euro enthusiasts called for, the latter desperately looked for alternative symbols of unity. When in 2012 Mario Draghi, the ECB’s newly appointed chairman, impressed bond markets with the rhetorical threat of unlimited action aimed at suppressing governments’ borrowing rates, many hailed his resolve as evidence that a long-awaited European polity had emerged. Two and a half years later, when he eventually set up a massive purchase program in order to combat deflationary trends, some went as far as to claim that the ECB had become the currency union’s de facto government.

These misplaced political expectations testify to the confusion over the nature and timing of quantitative easing in the Euro zone. At a time when the currency union and the European Union (EU) as a whole remain imperilled by severe competitiveness imbalances and the threat of political disintegration, the belief in the Central Bank’s omnipotence helps to delay inevitable choices on the euro’s future. The ECB’s action is, in turn, undermined by the fact that it serves an ailing political vision as much as a monetary target.

Before 2012, the ECB had been blamed for embracing the Bundesbank’s hawkish anti-inflationary doctrine. Then, Chairman Jean-Claude Trichet implemented it with a meticulousness that knocked out global markets, even more so when he later sought to reassure them… Under Mr. Draghi’s leadership, the ECB’s subsequent shift to monetary activism has helped to ease the EU institutions’ conscience, after their poor handling of the euro crisis. Meanwhile, the Central Bank has become hostage to a kind of political symbolism, as Europe fails to substitute a robust cooperation mode for the logic of an ever-closer union.

Not only might Brexit initiate a broader movement of disintegration of the EU, but fundamental divergence among founding members also prevents any long-term rebalancing from taking place in the Euro zone. What is often referred to as the global populist wave actually follows contrasting national patterns. In Europe, underlying political differences are being exacerbated by populism, along national lines. The ideological gap separating rising populism movements in France and Germany exemplifies this long-term trend, which the ECB must take into account but cannot actually offset.

Although both French far right’s Marine Le Pen and far left’s Jean-Luc Mélenchon share a common hostility to the euro with the Alternative for Germany (AfD), French and German populists diverge clearly when it comes to their broader economic approach. Whereas Le Pen and Mélenchon have adopted a statist stance purportedly informed by post-war interventionist policies, the AfD follows a particular version of “ordoliberalism”; a doctrine that was originally devised on the ruins of Nazism in order to prevent the government from exploiting economic institutions for political means. The current appropriation of ordoliberalism by the German far right centres, this time, on preventing transfers to the Euro zone’s south.

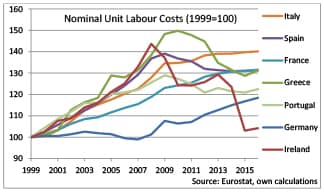

Germany has largely benefited from the euro’s creation. The successive governments’ strategic action to decrease nominal unit labour costs (by means of policies aimed at wage stagnation and low inflation more than productivity gains) has enabled German companies, from the early 2000s, to rapidly gain market shares over foreign competitors. After being deemed “the sick man of Europe” for several years as a result of its difficult reunification process, the country was eventually able to increase its trade surpluses vis-à-vis the rest of Europe and suppress unemployment.

After the euro crisis compelled many European countries into a severe adjustment, Germany’s exports growth began to increasingly rely on non-European markets, thanks notably to the euro’s weakened exchange rate. The idea of sharing the debt burden of southern European countries remains taboo to a vast majority of Germans. Berlin did not participate in the controversial bailout programs out of enthusiasm for a political ideal, but chiefly in order to prevent the currency union from falling apart in a damaging way for its own economy.

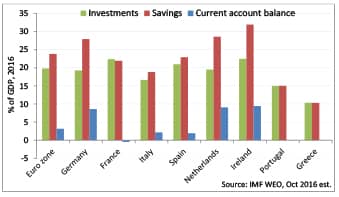

The country’s breathtaking current account surplus stands at nearly 9 percent of GDP (or almost $300 billion, more than China’s surplus). With total investments at 19% and savings nearly as high as 28% of GDP, this illustrates the distorting effect of this overall situation on the world economy. The generalization of this model to the Euro zone adds to its destabilizing impact. Against this background, Europe’s internal imbalances have quite understandably turned into a global concern.

Beneath Mario Draghi’s iconic status among EU and national technocrats, lies the hard reality of a profound divide between a reunified Germany and its western and southern partners, France and Italy in particular. This situation collides in the latter countries with the public administration’s dream of a grandiose political construct that would rid them of capital flight and exchange rate issues once and for all. Meanwhile, the single currency has provoked the opposite result. The ECB’s role as lifeline to the federalist ideal is part of a political strategy that fails to address the area’s fundamental flaws.

The ECB’s success in breathing some oxygen into the Euro zone has resulted as much from its massive monetary stimulus per se, as from the depreciation it has induced. Its purchase program was set up seven years into the crisis, at a time when credit supply had already bottomed out. While QE inflates the Central Bank’s balance sheet and excess reserves in the banking sector, it does little, in Europe’s context, to help reallocate funds toward cash-starved entrepreneurs.

The ECB loses leeway, as it is being excessively utilized as a political symbol by European governments and institutions that confront their own relegation and, at the same time, faces mounting pressure from Germany to wind down its monetary stimulus for domestic purposes. The embrace of monetary activism by a large portion of the European elite fails to dissimulate the fundamental fault line laid bare by diverging brands of populism.